Late payment on a loan - what are the consequences? What to do if there is a delay on the loan. Delinquency on the loan, what will happen.

Failure to repay a loan on time can have serious consequences. The scale of the problem depends on the length of the delay and the behavior of the debtor. One way or another, the information will be reflected in your credit history, and fines assessed by the bank can have an unpleasant impact on your wallet. So, let's find out what to do if the loan is overdue and is it possible to correct the current situation?

We assess and analyze the current situation

Important! Please keep in mind that:

- Each case is unique and individual.

- A thorough study of the issue does not always guarantee a positive outcome. It depends on many factors.

To get the most detailed advice on your issue, you just need to choose any of the options offered:

A conscientious borrower fearfully wonders what will happen if the loan payment is late. No one is immune from force majeure, illness, job changes and other difficulties that may cause delay. Bankers have many ways to influence debtors, and the preventive measure will directly depend on:

- The size of the debt.

- Length of delay.

- The client’s attitude towards the current situation (ignoring it or wanting to correct it).

Often, citizens who find themselves in a difficult financial situation hide from the creditor, avoid communicating with him by phone, and ignore letters and SMS messages. This behavior only adds to the problems, because the bank has the legal right to sell the problem debt to collectors or sue such a borrower. But clients who are ready to cooperate have the opportunity to get a deferment, refinance the loan, and other options. Everything is individual.

What to do if the delay is 1-3 days?

The first thing the bank does when the borrower is late is to charge him a fine. This action is specified in the loan agreement, which should be carefully studied before signing. In banking practice, there are 4 types of fines, namely:

- Fixed amount (in rubles).

- Penalty – percentage for each day of delay.

- The amount of the fine with an accrual total.

- Fixed interest accrued on the balance of the loan obligation.

However, most banks take into account that a small delay, for example one day, may be due to technical interruptions in the payment system. Or the payment receipt time is 1-3 days, and even if the client sends the money according to the schedule, but chooses the wrong repayment method, he may unintentionally violate his obligations. For example, payment via Russian Post may take up to 5 days.

Of course, this does not give the borrower the right to pay at the last moment and not be afraid of anything; on the contrary, money should be paid in advance to avoid possible delays. As for banks, it cannot be said unequivocally that in case of small delays they do not take any measures, although this is not excluded. Perhaps, if the client allows a minor delay for the first time, no punishment will occur, but if the creditor’s loyalty is abused, systematic omissions occur, the fact of a damaged credit history is inevitable.

Payment delay from a week to a month, what is the risk?

So, if a delay in loan payment of up to 3 days is not a terrible violation, then delays lasting a week or a month can cause unpleasant troubles and additional costs.

Attention: If you are in arrears on your loan, you don’t know what to do, contact the bank immediately and notify the lender about the reason for the incident. A timely decision will save you from cumbersome problems in the future.

Overdue debts in banks lasting 7-30 days entail worries in the form of active phone calls with constant reminders about:

- The amount of debt incurred.

- The amount of fines accrued.

- Further actions of the creditor if the current situation is ignored.

When talking with a banking specialist, it is advisable to voice the expected repayment date of the loan and its part. It is necessary to explain why the delay occurred and then the bankers may not call again until the day the payment promised by the borrower is made. Afterwards, if the loan payment is not made, the calls are resumed.

Overdue for more than 60 days – bank actions

If you allow a delay of up to 60 days or more, do not be surprised if the bank begins to act in the following order:

| Bank actions | Peculiarities |

| Intrusive calls, letters, SMS | As a rule, it is not the same specialist from the banking organization who calls, but different people - employees of the department for combating overdue debt. As a result, you will have to tell each of them about your problems again and again. |

| Selling debt to collectors | The agreement between the borrower and the bank specifies a clause regarding the possible transfer of rights of claim to another person if necessary. If the client has signed such an agreement, then there can be no claims. Otherwise, the decision can be challenged in court. Often banks do not sell the debt to collectors, but transfer it for proceedings with the debtor, having concluded an agency agreement with the collection organization. |

| Trial | A bank or collection agency can sue a borrower if it has the right to do so. This is the most terrible form of litigation with a debtor from a legal point of view. |

| Seizure and collection of property | Having received a court decision, bailiffs will begin to collect property from the debtor. If the borrower resists, law enforcement agencies become involved in the issue. |

Please also note that failure to repay a loan may result in imprisonment if the fact of fraud in obtaining money and malicious evasion of accounts payable is proven (Article 159 of the Criminal Code of the Russian Federation and Article 177 of the Criminal Code of the Russian Federation).

Additional solutions to the problem

When faced with the situation of being unable to pay your bills, contact your creditor. If there are compelling reasons for the current situation (loss of job, illness, business trip, etc.), the bank will definitely meet you halfway. The following solutions to the problem are possible:

- Loan refinancing. The program involves the borrower contacting a bank (you can choose another bank) to receive a special loan with a reduced interest rate, through which the current debt will be repaid.

- . The bank is reviewing the terms of the loan agreement. As a result, a deferred payment may be granted (“credit holidays”), the interest rate may be lowered, the currency of the loan may be changed (relevant for loans concluded in foreign currency), the loan term may be extended, etc. Restructuring stops the accrual of penalties and interest.

- . Based on Law No. 154-FZ, an individual has the right to declare himself bankrupt, meeting certain conditions: the amount of debt is over 500,000 rubles, overdue for more than 3 months, no criminal record, and insufficient value of his own property.

- Court. If none of the above options can be used, then a trial will help stop the increase in fines. The final amount to be refunded will be fixed. The assistance of a lawyer in this matter will not be superfluous.

If a collection agency starts taking over your business, don’t panic. Today, the activities of these organizations are regulated by law (Law No. 230-FZ). Any deviation from the norms of the document is a reason for filing a complaint with various authorities (prosecutor's office, police, Rospotrebnadzor, etc.), or going to court.

Delays on loans, unfortunately, have become commonplace in the lending market. According to 2015 statistics, the share of overdue loans for some banks reached 30-38%, and in the market as a whole, recent years have shown, although small, growth.

The main reason for delays is the instability of the financial situation of the borrowers or its deterioration; a person simply does not have the money to pay off the loan. At the same time, there is also a vicious practice in which the borrower, understanding the presence of difficulties and allowing delays, does not strive to resolve the problem in a timely manner. As a result, the amount of obligations increases due to the accrual of penalties, and the situation turns into a serious debt burden that the debtor cannot cope with on his own.

If there is arrears, the main task is not so much in deciding how to repay the loan, but in choosing the optimal way to resolve the debt problem. If there were temporary financial difficulties that led to delays, but they were overcome, it is enough to simply pay off the resulting debt and enter the normal schedule for fulfilling obligations or repay the loan in full. It is much more difficult to resolve a problem when temporary difficulties have become permanent. Here you need to think about how to negotiate with the bank and jointly find the best way out of the situation.

How to resolve a situation with an overdue debt before the matter reaches collectors and the court

The problem of overdue loans is a problem for the entire banking sector as a whole. Moreover, the formation and increase in the share of overdue loans, and, accordingly, the increase in the share of problem debts, negatively affects the financial position of the bank, forcing a mandatory increase in the amount of funds reserved for possible loan losses. Thus, you should not think that the bank from which you took out a loan and made late payments will not, under any circumstances, make some concessions in order to create acceptable conditions for the borrower to solve the debt problem.

The easiest way to resolve the situation with repayment of overdue debt- agree with the bank on a mutually beneficial settlement of the issue, before everything comes to the involvement of collectors or judicial review. The debt will still have to be repaid, but it’s better without unnecessary nerves, financial losses and time wasted.

Resolving the problem may look like this:

- At the first stage, you should obtain a certificate and debt calculation from the bank in order to carefully analyze, assess the amount of debt and think through possible ways to solve the problem.

- Then you need to come to the bank (just come, not call), explain the situation and ask to consider the issue of deferment/installment payment with a revision of the schedule, for which you should write a corresponding application, attaching documents confirming the presence of financial problems. Among the possible options for resolving the situation, both the borrower and the bank may offer other methods of debt restructuring. For example, sometimes a credit institution is even ready to refuse to demand penalties or to reduce their size. In some cases, the bank may offer loan refinancing.

- In a situation in which you have the opportunity to repay an overdue debt, on the basis of a bank statement, prepare a corresponding application, indicating the amount that you plan to contribute to repay the overdue loan, and be sure to precisely this purpose for its payment, so that the transferred funds are not directed , say, to pay off a penalty. Such a resolution of the situation is usually resorted to when there is an intention to enter into a normal mode of fulfilling obligations according to the original schedule. The same method is suitable if you want to completely close the loan, but here you should be prepared to pay off all fines.

- Relations with the bank regarding the settlement of the problem with overdue payments must be of an official nature, that is, all certificates, calculations, new agreements must be drawn up in writing, and the documents must be dated, sealed and signed by the responsible persons. If you repay the loan partially or completely, be sure to keep statements about this and payment documents. In a situation where an overdue loan is fully repaid, it is extremely important to obtain a certificate stating that the debt has been fully repaid and the bank has no claims against you. This will help avoid problems if a credit institution suddenly misses something, loses something, or wants to recalculate late fees - such cases occur in practice.

Pre-trial settlement is only suitable for situations where:

- the borrower has something to offer the bank for a mutually beneficial resolution of the problem through debt restructuring;

- there is an opportunity to at least partially repay the debt, or better yet, to find funds to fully repay the loan;

- The bank is ready to make concessions, having entered into a difficult financial situation of the borrower, and revise the schedule with the establishment of deferment or installment payments, including without the imposition of penalties.

If there are no funds even for the monthly payment and (or) the bank does not make concessions, then, unfortunately, only the court can finally resolve the problem. Moreover, most likely, the borrower will still have to deal with collectors, contacting whom has already become standard banking practice.

How can it be beneficial for yourself to resolve a situation with an overdue debt if the bank has gone to court?

When the situation comes to court, the following must be considered:

- Today, courts consider cases of debt collection very quickly. A simplified procedure for issuing a court order for collection is often used, which is both a decision in the case and an executive document. The order can be issued in absentia, that is, without the participation of the debtor, as a result of which the borrower is faced with the fact of the impending seizure of property, and often the impossibility of appealing the order due to the expiration of the time period allotted for this. To avoid negative consequences for yourself, be sure to control the development of the situation.

- Try to find the opportunity to at least consult with a credit lawyer. This must be done after the delay has occurred in order to clearly understand what can be done, what should not be done and how, in general, to behave in the current situation. Ideally, of course, it is better to hire a lawyer for a lawsuit.

- If you are summoned to court, do not ignore the possibility of your participation in the process. You have a real and very high chance in court to obtain an installment plan/deferred payment on the loan by presenting evidence of a difficult financial situation, difficult life situation, etc. In addition, it is possible to challenge accrued penalties, minimize them or completely exclude them from banking requirements. If there are grounds, the courts quite often make such a decision in favor of the borrower.

The bank's appeal to the court does not exclude the possibility of reaching a settlement agreement with the creditor. Therefore, when participating in a lawsuit, you should not give up trying to resolve the problem by agreeing with the bank on debt restructuring. However, the greatest likelihood of coming to a profitable solution in this case is only with the participation of a qualified lawyer who knows exactly how and in what manner to negotiate with the bank.

Open arrears prevent you from obtaining a loan. But in rare cases, banks meet halfway and provide money on special conditions. When making a decision on an application, banks must check the borrower’s solvency. The main indicators of reliability are good credit discipline and timely fulfillment of financial obligations.

What are delays and how do they affect

According to the law, credit institutions are required to transmit information about overdue payments to the BKI as early as the 5th day. But in fact, banks delay this information for up to 1-2 weeks or more. As obligations are defaulted, the status of the debt is updated.

The loan decision depends on the nature of the delay:

| Type of delay | Peculiarities | Bank decision |

| Technical | Payment delays may occur due to technical and other failures in the bank's operations. The payer makes the payment on time, but it is reflected in the credit history after 1-2 weeks. | In this case, the client is not included in the category of malicious debtors, and the delay does not in any way affect the decision of the creditors. |

| One-time short-term | A one-time open delay is not considered a systematic violation. | Some banks are ready to approve a loan if the applicant has one delay of up to 10-15 days, but in the past he has regularly repaid his debts. |

| Long-term | Open overdue debts of more than 1 month are regarded as deliberate evasion of obligations | With such marks in the dossier, it is almost impossible to get a loan from a bank (especially if this is not an isolated case). |

How to convince a bank of your reliability?

Delays are possible even for responsible borrowers, for example, due to delayed salaries or unexpected medical expenses. A new loan may be needed to cover current overdue debts. This is not the best option, since such a scheme almost always leads to a credit pyramid - new loans to pay off old debts.

If it is not possible to borrow from friends and going to the bank is inevitable, try to convince the lender of your reliability:

- indicate all sources of income;

- Additional income confirm with relevant documents - a certificate in the bank form, statements from bank accounts and electronic wallets, a lease agreement for your own real estate, a certificate of receipt of dividends, interest on deposits, etc.;

- provide telephone numbers of your manager and close relatives;

- Bring a solvent guarantor with official work.

Pledge of property will allow you to receive it even if you have overdue debt. The following are accepted as collateral:

- securities.

Such a step is permissible only in cases of extreme necessity.

A secured loan involves a high risk of loss of property in case of failure to fulfill obligations.

Refinancing

It is recommended to apply for the service before you fall into arrears, if you already understand for sure that you will not be able to cope with your current obligations. In some commercial banks, refinancing is available even if there is an overdue debt.

Advantages of refinancing for the client:

- allows you to avoid or prevent the growth of arrears;

- reducing the amount of monthly payments by extending the term and reducing overpayments;

- convenient payment schedule;

- You can additionally receive a certain amount of cash in your hands;

- all loan obligations are combined into a single agreement.

The bank conducts a standard check of the applicant, assesses credit history and income. The application is reviewed within several days. If the decision is positive, the client signs a new loan agreement:

- documents for all loans are reissued;

- if the initial loan was secured by real estate, the right to receive the property in the event of non-repayment of the debt passes to the new bank;

- the creditor transfers funds to pay off “old” debts;

- the borrower terminates cooperation with the original creditors and begins settlement under a new agreement.

If you refuse, contact other organizations. Refinancing services are available not only in banks, but also in microfinance organizations.

Where will they give you a loan if you are in arrears?

Some banks allow one short delay, because they understand that such violations happen even to already reliable and solvent clients. Lenders are willing to turn a blind eye to small flaws in the CI if the applicant meets all the requirements and has sufficient income.

The list of banks loyal to the damaged CI includes:

- — from 9.9% only with a passport;

- - from 9.9% even with poor CI;

- — from 7.9% for 1 document;

- — with a damaged credit rating or zero history of 15%;

- — from 14% with an online application;

- - from 12% from 18 years of age and only with a Russian passport;

- — from 11.5% with quick consideration of the application;

- — credit doctor program specifically for CI correction.

You can get a loan from most of the listed organizations. Despite this, it is recommended to bring with you a complete set of documents, including certificates from work.

Citizens with a damaged history and open arrears will have to pay an increased rate - in the range of 20-50% per annum.

Insurance

If your credit history is far from ideal, agree to insurance services. Minus insurance, you will receive a smaller amount, but the chances of approval are much higher.

Typically, loan officers offer to take out life or health insurance. Within 14 days from the date of conclusion of the transaction, the client has the right.

Credit cards and overdraft

If the payment is overdue for a long time, it makes sense to apply for a credit card. The requirements for this product are minimal. However, the interest rate is higher than . In addition, you will have to pay for annual maintenance and for withdrawing money from an ATM. As an option, you can apply for one that allows you to withdraw money from an ATM without commission.

To save money, get a card with a grace period during which you can use money for free.

Overdraft is an alternative way to obtain credit funds. But it will take some time. The client issues a debit card and regularly tops up the account within 2-3 months. Regular account transactions increase the level of trust. The client may ask to open a credit line on this card, that is, connect an overdraft - the ability to withdraw more than is in the account. This turns a debit card into a credit card. By making timely payments, you can continue to qualify for more profitable products.

Where else to apply for a loan with arrears

Loan refusals are not a reason to give up - apply for a microloan. MFOs are less demanding of borrowers and provide funds to almost everyone who applies, including those with a bad payment history and unofficial income.

- — one of the three most popular microfinance organizations in Russia. Normal rates from 0.76%, fast delivery.

- — the first loan is issued without interest. Below are the standard rates.

- — also promotions for new old clients. You don't have to pay interest.

If none of the options listed above suits you, contact a credit broker. These are professional intermediaries who help you find the best option with reasonable requirements, collect the necessary documents and understand the terms of the contract. Conscientious brokers charge based on the results of their work.

If you are promised a 100% result and require an advance, you are most likely dealing with scammers.

Don't agree to an advance. Pay only when you achieve results.

For the survey to work, you must enable JavaScript in your browser settings.

By taking out a loan, the borrower expects timely repayment. Unforeseen life situations can throw you out of your usual rut, and a person realizes with horror the occurrence of overdue loans, not knowing what to do in this situation. The main thing is not to create panic and analyze all possible options. There will definitely be a way out!

Absolutely any borrower who has problems at work, their home burns down, or someone in their family becomes seriously ill and requires expensive treatment can become insolvent. Therefore, if everything is fine today, and a person is completely confident in his financial capabilities, then he can take out a loan, but just in case, you should find out what a delay is and what it threatens.

Borrowing banks understand overdue debt as a certain amount that the borrower has not paid to the lender on time. As a rule, after the established payment deadlines, penalties and fines are automatically charged. The bank sets and stipulates the amounts in advance in the agreement, which it is advisable to study in detail when signing. Then the bank files a claim with the court for overdue credit, and the borrower has a completely reasonable question - what to do.

As a rule, people encountering the banking system for the first time begin to panic and hide from bank employees and do not respond to written warnings and calls. This behavior is extremely undesirable, all this will only aggravate the overall situation, and the bank will have a reason not to trust the client and be more harsh with him.

In any case, the borrower needs to maintain friendly relations with the bank and agree to a joint solution to the problem. First of all, you need to understand what may follow and how other borrowers find a way out.

Conventionally, all debts to the bank are divided into certain types that fall under the classification of overdue periods. Depending on how difficult the problem is, the bank may offer its own ways out of the current situation.

No more than a month overdue

The simplest and somewhat harmless debt for the borrower is considered to be debt whose terms do not exceed one month. During this period, usually the banks themselves systematically call the client, send appropriate letters about the need to repay the outstanding loan arrears, or offer to come to the branch in person.

When the client manages to correct the current situation as soon as possible, this misunderstanding may not affect the credit history, and in the future the application for a loan from this bank will be considered positively. However, the penalties provided for in the contract are imposed, and for days of delay there is a penalty. In general, the amounts are, of course, tiny, but the fact itself is already unpleasant, because the bank takes such clients under its close control.

To solve the problem, it is enough to go to the bank and write a statement about the possible deadline for repaying the debt. The payment date must be specific. It is selected based on the client’s capabilities, taking into account the reason that led to this problem. The payment amount is clearly specified; if there is a large debt, partial payments are possible, but only with documentary evidence of the borrower’s temporary insolvency.

In such a situation, basically all banks meet their clients halfway, any problems are resolved taking into account the interests of both parties, the main thing is not to hide and prepare supporting documents.

Debt up to three months inclusive

It is somewhat more difficult to deal with loan debt if the non-payment period is three months. In such a situation, it is best to partially repay the debt, at least in small amounts. The fact is that in banks this is provided for by law. If employees until now have not been able to contact the borrower and find a joint solution to the problem, then they will probably find contact with guarantors, relatives and file an application for recovery in court.

When the amount of debt increases sharply and reaches half a million rubles, then litigation cannot be avoided. A careless attitude towards obligations can lead to the bank filing a lawsuit, which, in turn, will consider it necessary to seize some property or offer to sell it and pay off the loan.

If the company shifts the repayment of the loan onto the shoulders of the guarantors, then this is the worst option for the borrower: not only financial “punishment” of the people who once came to his aid, but also damaged personal relationships. In addition, when the guarantors pay the debt, they have the right to sue the borrower to recover the funds paid and legal costs.

In this case, in order not to aggravate the situation, the client must periodically report on his solvency. A dialogue with the bank will allow you not only to gain time, but also to come to an agreement.

If there is a 100% possibility of repaying the balance of the originally borrowed amount, that is, the principal debt, the borrower may have penalties reduced or even canceled. Interest will be recalculated, the loan itself will most likely be extended for a certain period, and accordingly, monthly payments will also be significantly reduced.

What does the bank offer?

Often in such cases, banks offer to restructure the overdue loan. This means that not only the terms, but also the amounts of payments change. It is possible to write off a partial debt or a banal exchange for a certain type of property. But such a procedure is considered real only if the borrower has experienced specific changes in living conditions, again confirmed not only by the application of the applicant, but also by the relevant documentation.

It is important that the client has not previously been blacklisted and his credit history is positive. Otherwise, the loan may be denied. The restructuring process itself should be viewed positively, because it is based only on the client’s interests and abilities to repay the debt, which does not negatively affect the borrower’s history.

Five months overdue

When a borrower manages to remain a debtor to the bank for five months, then, apparently, he constantly cooperated with the bank and looked for joint ways to resolve the situation. Banks always remain lenient towards such clients and make all sorts of concessions, allowing them to pay off loans based on possible resources. Usually, over such a long period, debtors clearly assess the problem and, trying to find a way out, find opportunities to improve their financial situation and begin making payments at least in the minimum amount.

In such situations, the main thing is not to get lost: come to the bank at the first invitation, provide the necessary documents, write applications to extend the deferment, and the employees of the financial institution will always meet you halfway. Otherwise, such lending will end in failure.

Six months overdue on loan

When the loan is overdue for more than six months, but the borrower has been “active” and has been in close communication with the bank throughout the entire period, there is nothing to fear. Reminders about debts will continue to come from the bank - this is a common formality. You still need to partially repay the loan, keep relevant documentation, and provide written confirmation of your solvency. Understanding the dangers of delay, try to close it as soon as possible.

When the problem is resolved, albeit slowly, the banks make concessions in this case as well. The main thing is for the borrower not to lose information about employees, with whom negotiations were conducted, and documents provided by the bank.

Overdue - a year: what to do

It is more difficult with a long term debt. for example, you need to sound the alarm when the loan is overdue for a year or more. What to do in this case is not always clear. As a rule, many begin to panic and hide from representatives of banking organizations, not thinking at all that they are only aggravating their own situation.

In this case, the loan debts will not go away, they are growing rapidly, and the bank is preparing the necessary documentation for the client to submit to court. This happens even better. It’s much worse when the bank “transfers” debts to collectors, and then the problem becomes almost unmanageable.

Therefore, we need to make contact and try to resolve everything peacefully. Otherwise, it is difficult to say what communication with collectors will lead to. Their manner of speaking is tough and their attitude is unyielding. It is difficult to say how to behave and what to do if the bank has involved such services in “knocking out” debts. When coming into contact with them, you must remember that the found way out of the situation will solve the problem in favor of the borrower. The main thing is not to remain idle and take some measures to change your financial situation.

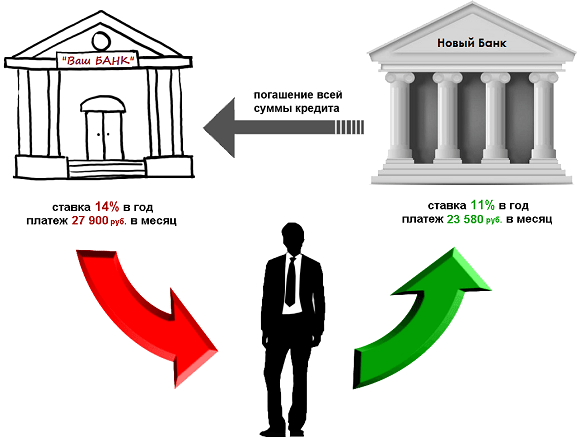

Loan refinancing - a quick way out of the situation

When the terms of the debt are extended, the interest only increases, but the debt itself does not decrease. If you are not sure what to do, you should consider refinancing. The bottom line is that the borrower can take out another one to repay this loan and cover the first one. In this case, you can find more loyal and gentle conditions. You should seek help both from another bank and from the same one where the loan was made.

If the decision is positive, the borrower benefits greatly. A new bank loan allows you to postpone time. If you manage to choose this option, then it is possible to reduce interest rates. The most important thing is that lenders will “lag behind” the borrower for a while. Even if he had several credit debts, now there will be only one. This is the best option in such a situation.

Which bank will refinance the loan?

The procedure is very common, and basically all large banks agree to it. You can complete a similar procedure and repay “straining” loans at Sberbank of Russia, VTB 24. This service is provided by Rosselkhozbank, Uniastrum Bank, B&N Bank and many other organizations. The new loan is immediately transferred to the bank where the debt was incurred; the remaining funds are issued to the client and can be spent at his discretion.

However, we must remember that a new loan does not solve the problem as a whole, but only slightly alleviates the situation. If debts continue to arise, all difficulties will arise again. A clearly damaged history will aggravate the borrower’s problem.

You also need to understand that new conditions may not always be beneficial. In order not to create even more difficult situations, it is better to contact some other financial institution. Be careful when taking out new loans, because today it is easy to run into scammers who offer instant loans online at incredible interest rates, digging the borrower into an ever-deeper hole of debt...

You can try to re-borrow from someone, pay the bank at least the main part of the debt. Then the whole procedure for the borrower will change dramatically, there will be an opportunity to fix something, delay time, or resell something.

There is nothing wrong with bank loans. But before you take out a loan, you need to clearly weigh your own financial situation. Consider not only your current financial situation, but also look a little further ahead, try to take into account the economic situation of the country and think about how this can affect everyone specifically! Whether a person will be able to pay such amounts tomorrow and repay the loan on time is up to the person to decide. Often people “drive” themselves into hopeless situations, only once incorrectly assessing their own strengths and embellishing their capabilities. If you are in arrears on your loans, answer the questions “what to do” and “what to do”, guided by the knowledge gained in the article, in order to get out of the current situation without any problems.